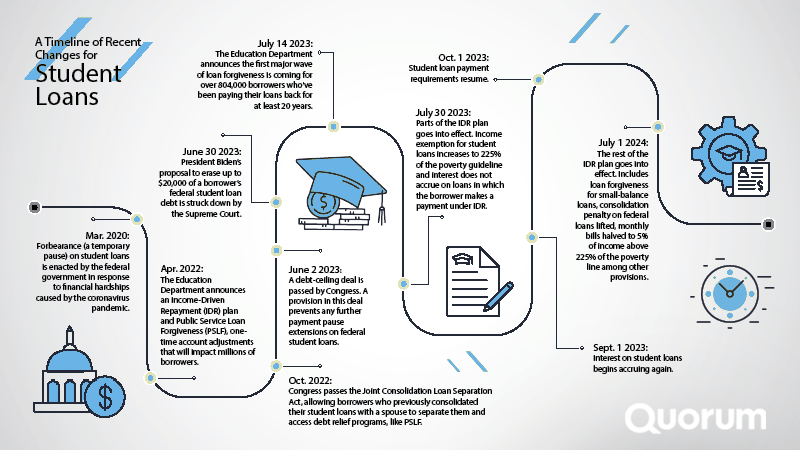

According to a new study by TransUnion, millions of Americans will have to start making payments of at least $200 (with one in five making $500 or more) when student loan payments resume this October.

A student loan isn’t like a car loan, where you buy the car and pay it off over five or six years with one set interest rate and one set payment.

Instead, it’s like buying a car every year of college: Each year, you take out a new loan with a new interest rate and a new repayment schedule. So by the time you graduate, if you’ve borrowed money each year, you will have at least four different loans (more if you’ve gotten an advanced degree).

If you have student loan debt, you aren’t alone. Total student loan debt among Americans is $1.75 trillion, with the average borrower owing $28,950.

When you combine the loan payment with other expenses like housing, food and transportation, you might wonder how you will escape the debt.

While paying the balance due may seem like running a marathon, you may be able to reach the finish line faster by following the tips below.

1. Verify what you owe.

Creating a student loan repayment strategy starts with figuring out just how much you owe and to whom. A good place to start is creating an account with the National Student Loan Data System, a central database for federal student aid. It receives data about your loans from colleges and universities as well as federal lending programs.

The system will show your outstanding loans, their interest rate and balance. It won’t include non-federal loans, such as from a local financial institution, so in order to get a full financial picture, be sure to also obtain a copy of your credit report, which will list any private loans you might have taken while in school that were deferred until graduation. Your credit report can be requested once a year at no charge from each of the three credit-reporting companies—Equifax, Experian and TransUnion—online at www.annualcreditreport.com.

Once you’re armed with this knowledge, make a list that details your interest rates and loan balances.

2. Evaluate your income.

Next, set aside loan balance list and make a different one: your income and your debts. Include all of your fixed bills, such as your rent, car payment and insurance, and estimate how much you spend on groceries, clothing, dry cleaning and such each month. (Don’t forget to budget for savings and retirement account contributions, too.) Add in your incidental spending by reviewing expenditures on your debit card or through any payment apps you use.

For the most accurate look at your income, keep a spending diary for the next 30 days to see exactly where you spend your money. Compare that with your income over that same period. That will give you a full financial picture, show you how much you have left at the end of each month, and allow you to create your loan repayment strategy.

3. Pay more than the minimum due.

For illustrative purposes, let’s say your student loan debt looks like this, two years after graduation, with eight years remaining on the standard 10-year repayment schedule for federal loans (the payment length varies for private loans):

Loan 1: $719.16 at 3.760% fixed-rate interest

Loan 2: $4,632.75 at 4.290% fixed

Loan 3: $2,840.55 at 4.660% fixed

Loan 4: $5,027.52 at 3.760% fixed

Using a student loan calculator, you determine that the combined minimum payment for these loans is $162.01 per month. Your monthly budget shows you can afford to pay double that amount (which will accelerate your repayment plan, and save you money in interest).

Where do you put that extra $162? You can assign it to a specific loan rather than spread the money over each loan. By assigning it to Loan 3, you’ll be speeding up the payment on your highest-interest loan, and saving money in interest. Once it’s paid off, you will re-allocate that extra $162 to the next loan in line.

While it’s usually wise to pay the highest-interest loans first, given the comparatively small balance on Loan 1, people occasionally choose to pay off the small balance first for the psychological boost and motivation it can provide. Once the small loan is paid off, extra money is then shifted toward the higher-interest Loan 3.

4. Other ways to increase your student loan repayment.

If your budget doesn’t allow you to put additional funds toward your payment, or if you’d like to find a way to pay even more, you’ll have to get creative with coming up with some extra cash. Some are easy; some require sacrifices.

- Put extra money toward your loans. Receive a tax refund? Bonus? Get a raise? Make a lump-sum payment or increase your monthly payment whenever possible. A $25 a week increase in your take-home pay is $1,300 a year that can go toward your student loans.

- Consider refinancing your loans, especially your private ones. Refinancing your loan at a lower interest rate can reduce your monthly payments, allowing you to put more money toward your loan in the long run. While you can replace your federal loans with a private one, be aware that federal loans come with some protections—you could get a lower monthly payment if you run into financial difficulties, for instance—that aren’t available with non-federal loans.

- Sell unused items. Your career might mean you don’t have time to play video games anymore, or you just might not use that expensive handbag you received as a gift very much. An influx of a few hundred dollars from selling some unused things online could fund an extra payment on your loan.

5. Think twice before choosing these student loan repayment options.

The sooner you pay off your student loans the better. But we all know that making even the minimum payment can be tough under certain circumstances.

The federal government recognizes some student loan recipients might have a hard time making their monthly payments, either on a short- or long-term basis.

If you have federal loans, you can apply for an income-driven repayment plan that is based on your ability to repay. This option might best be limited to people who otherwise would be at risk of defaulting on their loans. While your monthly payment will fall, it will increase your repayment time from the standard 10 years to 20 or 25 years, depending on the specific plan selected, thus most likely increasing your total interest paid. (Learn more about the new income-driven repayment plan, SAVE, in our article which has cut monthly undergraduate loan payments from 10 percent of discretionary income, to 5 percent).

The government also allows you to apply for forbearance or deferment, which allow you to postpone your student loan payments. While it sounds attractive, this option should be used only on a short-term basis, such as while paying off an emergency car repair, because interest will likely continue to accrue. Only deferment allows you to defer interest and you must have a major life event occur, such as a job loss, to qualify.

You didn’t earn your college degree overnight, and you won’t pay off the loans overnight, either. But with a solid repayment strategy, and by staying on top of how much you owe on a regular basis, you’ll be able to whittle down those loans and pay them off before their scheduled end date.

Comments Section

Please note: Comments are not monitored for member servicing inquiries and will not be published. If you have a question or comment about a Quorum product or account, please visit quorumfcu.org to submit a query with our Member Service Team. Thank you.